As public adjusters, we negotiate with insurance companies every day. We see firsthand the reasons they cite for denying claims by policyholders – both homeowners and businesses. To help you position yourself for a successful claim process, we compiled the top reasons insurance companies cite for denying a claim.

1. Water seepage

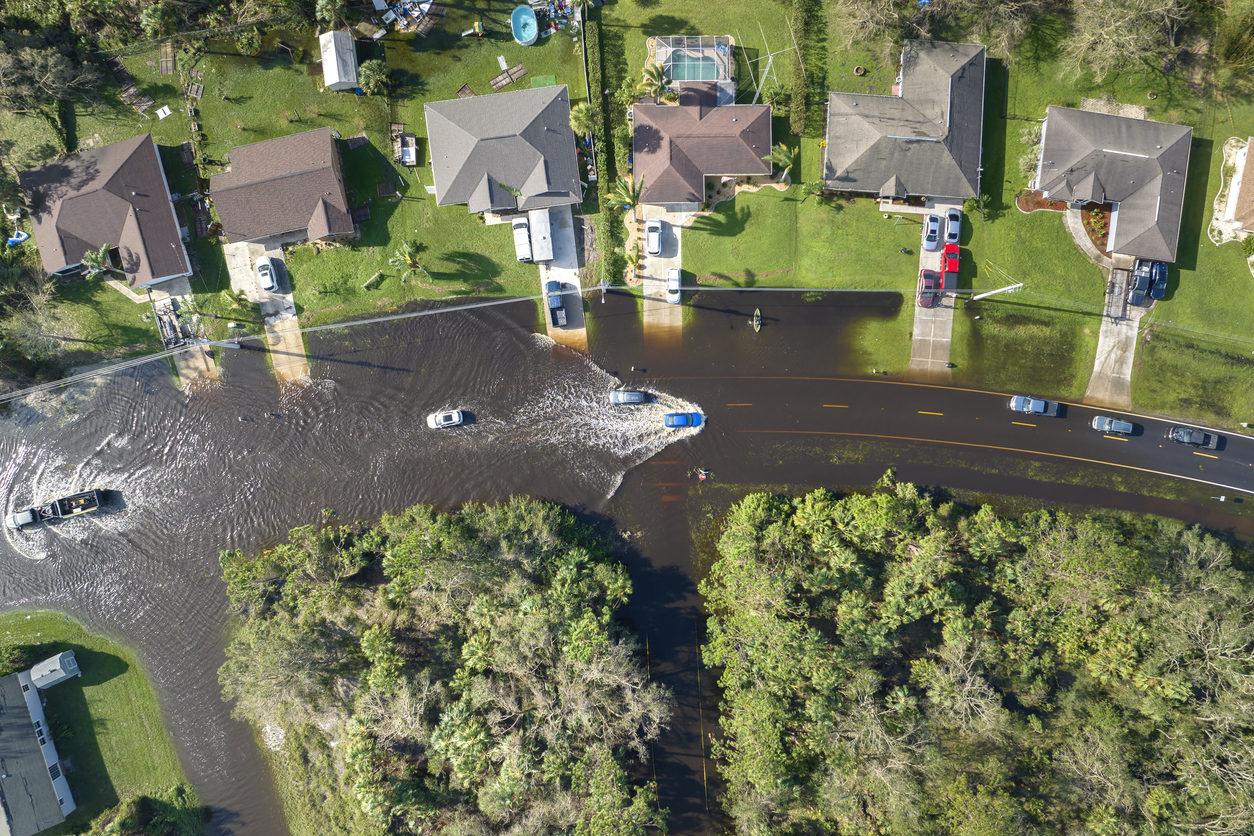

Seepage of groundwater into your house is NOT a covered event in a standard homeowners policy. In your homeowners policy, the language is very clear: once rainwater hits the ground, it’s considered surface water or groundwater. This means that if water seeps through your foundation, you have no coverage AT ALL. On the other hand, if there’s a heavy rain and water seeps in through walls that are above grade, you will have coverage for that (NOTE: this is only true for an all-risk homeowners policy).

Both the Business Owners and the Commercial Property policies contain this exclusion for seepage and groundwater. But there is a key difference – in a commercial application, for any interior water damage to be covered, the roof or the exterior of the building must first be damaged by a covered cause of loss. So, the roof must first be damaged. Say there is a windstorm and a fallen tree slices your rubber roof. If the windstorm lifts a section of that damaged roof and allows water into the envelope, that’s a covered event. Rainwater seeping into a building around a door or window is not a covered loss in a commercial policy.

2. Frozen pipe vs. burst pipe

In general, water damage from a burst pipe will always be covered under both a homeowners and commercial insurance policy. Things can get tricky, however, when frozen pipes are involved. For the most part, frozen pipes will NOT be covered, unless you can demonstrate that you maintained adequate heat. Which brings us to…

3. Failure to maintain heat

Most insurance policies — both homeowners and commercial – require that you take “reasonable care” to maintain heat in the building or house, or that you “shut off the water supply and drain all systems and appliances of water.”

If you are away on vacation and your pipes freeze – but you left your heat at a reasonable temperature and the boiler failed – your loss will be covered. But if you were late for that flight to Florida and forgot to leave any heat on, your insurer can refuse to cover the loss.

Please note that these tips are based on standard homeowners insurance policies. It is very important for you to read your individual policy as forms vary drastically. Should you want SMW to review your policy, please contact us to discuss.

Be sure to check back for valuable tips and information. And if you need assistance in resolving an insurance claim, call Swerling Milton Winnick.